Banking Failures with a Side of CBDC?

As we highlighted at the end of last year, the banking failures we are experiencing today are not unexpected given the total lack of accountability from senior executives at these institutions...

Welcome back Cignals family! Our dev team has been putting in immense work that we could not be more proud of! As of today, I’m happy to announce that our live-trading enabled DOM (depth-of-market) has gone live (in beta mode) for our advanced tier subscribers to test using Binance Futures! Super proud that this moment is finally a reality, as it has long been an ambition of ours to deliver! Truly excited to continue adding additional exchanges on the DOM for our advanced-tier users to take advantage of! If you haven’t subscribed to Cignals yet, we recommend grabbing an advanced-tier membership which gives you access to a whole host of perks, including live trading, but more importantly, you will be grandfathered into our legacy-tier which grants you access to all of what we have planned in the future (even features that will be offered at a higher price point) for today’s low price of $79/mo.

The legacy tier started in 2021 at $50, and we made a simple promise back then to our first users… Stick with us as we grow, and you will never pay more for any services we offer in the future as a token of our appreciation! Today, we are extending that same promise and token of gratitude to our current advanced tier subs, you will never pay more for any features we offer at a higher price point for the life of your advanced subscription! Your OG tag (discord tag) will grant you access to the entire platform unrestricted, even if tiers, pricing, and offerings change in the future. The OG discord tag will be retired after Labor Day Weekend 2023, and the legacy tier will no longer be available. Remember it’s valid for the life of your subscription and can be paid in full every year at a discounted rate.

Summer vibes are finally here in the Northeastern United States! It’s a time when most participants of financial markets take a step back from the hectic day-to-day operations to enjoy the warm weather, spend time with family & friends, as well as limit their exposure to screen time. As a result, markets may begin to feel slower toward the end of June (we write a yearly report called ‘The Doldrums of Summer’ explaining how to navigate this) until roughly Labor Day Weekend. So far the spring & summer season has started with a bang!

If you recall, we previously went over the very obvious signs that banking stress was a real problem that many MSM pundits and analysts were reluctant to address. We highlighted the increasing number of banking institutions holding onto toxic assets, using the Feds discount window, along with record reverse repo usage, and pointed out that this doesn't exactly point to a robust and healthy economy. Especially given the fact that banks are holding a ton of low-yielding bonds to maturity and sitting on massive unrealized losses in today’s high-yield world. This is why we’ve seen regional banks such as Silicon Valley Bank, Signature Bank, and First Republic go under when depositors lined up to get their money out by the thousands.

Figure 1 above shows a weekly chart of the SPDR KRE (regional banking ETF) and the yellow circle is where we started calling for increased awareness around issues sparking multiple bank failures. As you can see, the index was trading at roughly double its current price during that time. There have been many more whispers of regional banks under pressure with deposits slowing heavily over the last 60 days. Fear not, as the treasury has backstopped all of these institutions via the Bank Term Funding Program and proposed removing FDIC limits on insurance for deposits. In essence, they are fomenting moral hazard of epic proportions at the highest levels of the American banking sector. What incentive does a bank have to manage its risk, if they know the treasury (and ultimately the Fed) is waiting in the wings to save the day?

Let’s also put aside the fact that Signature Bank most likely did not need to be seized by New York State regulators & handed off to the FDIC. Ostensibly, it appears this was most likely a hit job on one of the few remaining banks in the United States that openly worked with cryptocurrency companies (and one that worked closely with former POTUS Trump). Something seems amuck here considering that Signature was acquired by NYCB and forced to leave behind its crypto business as part of the acquisition terms. For a bank that was supposedly about to fail due to customers asking for their money back, it seems a bit ironic that NYCB would be the firm that ended up with the bulk of Signatures assets.

Say you wanted to pull $50,000 out of NYCB, do you know how long you’d have to wait for them to obtain that type of money and have it on hand? About ten days or longer, and they would subject you to a lot of questioning as to why you wanted to take your own money back from them. If you wanted to cash a $5,000 or greater check written from a business account that was held at NYCB and you bank with one of the larger US banks (such as JPM, BoA, Citi) do you know how long the hold period is on that check? Roughly two entire weeks, so your bank can “ensure that NYCB has the funds on hand and is able to transmit it without issue” which is astounding. Operation Chokepoint 2.0 seems to be working according to plan, which will undoubtedly help usher in a cashless society, and of course, the first CBDCs in the United States. Keep in mind, all of this comes within weeks of the Fed Now pilot program set to be released.

TLDR on Fed Now is it’s essentially a 24/7/365 instant payment service, akin to Zelle that has no limits on what you can send. Unlike Zelle which is managed by a private company and banks opt-in, the Federal Reserve controls this system entirely. As a thought experiment, let’s assume you wanted to issue a CBDC and force people to use it. Cash and cryptocurrencies such as Bitcoin provide a way for individuals to transact relatively freely with little constraint. Your first step would be to weaken the crypto space and make it look like a systemic liability in the eyes of the general public, which wasn’t all that hard given the FTX & Signature Bank fiasco. Next, you’d need to start nationalizing the banks without actually nationalizing banks. Killing off small regional banks and credit unions one by one is a great start, having them gobbled up by the likes of JPM for pennies on the dollar is even better.

What about the larger banks? Well, you’d incentivize them to gobble up as many low-yielding treasuries as humanly possible and hold them to maturity. In the process, make sure you ignore all of the economic data pointing to vast money printing coupled with 0% rates causing 50-year high inflation, allowing the economy to “run hot” for an extended period of time. After all of your FOMC insiders sell their portfolios off at cycle highs, pull the rug out on everyone & raise rates by 525 basis points in under 18 months. Finally, after working on the rails of a CBDC (Fed Now) behind the scenes, you’d start to slowly roll it out and openly test it. There will likely be issues relating to fraud that need to be dealt with before this system can be widely used in every sector of the economy. This live testing period will also measure how much demand there is from the public for this type of system, and more importantly, how the public uses this system.

If all goes well during testing, and there is decent demand for this type of service, it wouldn’t be far-fetched to see larger banking institutions have solvency issues in the event of a high-yield world rocked by a severe recession. Taking a page from the 2008 playbook, let’s say that the Fed doesn’t react quickly and lets rates stay where they are, banks would be sitting on massive losses and be in need of emergency access to cash as redemptions started to pile up quickly. There’s a very real possibility of a bail-in situation where depositors in these theoretical scenarios would be issued a CBDC (hypothetically) in order to be made whole. Larger banking institutions would likely be consolidated even further until there’s only a handful left standing. There would be mass panic, and no time for the average normie to assess the situation of being given a digital currency issued by the central bank directly. Eventually, the use of this money would come with strings attached (social credit scores anyone?) and deeply negative interest rates could be used effectively without the fear of causing further bank runs.

Obviously, this is all speculation, but we’ve been writing about this possibility for well over a year, and it seems like all the pieces are in place. Let’s not forget that the world is now de-dollarizing at a massive rate. Saudi Arabia is ready to start selling oil and have it settled in Yuan which is a major signal about the Greenback’s dominance in world trade coming to an end. India has been purchasing oil from Russia and paying in Roubles (as well as other FX), circumventing the harsh sanctions placed by the United States & NATO. China has been paying for gas and oil from Russia in Yuan and Roubles for quite some time already which is another major sign that the global south and BRICS+ may eventually follow suit (or even form their own currency). Let’s not forget that Chinese banking institutions have moved away from the SWIFT system as well and developed their own interbank messaging system, CIPS, while Russia has the SPFS system in place.

Obviously, the United States Government sees the writing on the wall and wants to limit the way Americans use cash and Bitcoin so that regular citizens cannot circumvent the last remaining power the USD has left. The only way to do this is to issue a CBDC and force people to use it. Keep an eye on this over the coming months, as a recession is almost inevitable and should kick this type of scheme off in earnest. I could be completely wrong, and frankly, I hope I am wrong… Something hasn’t smelled right for quite some time, and it appears the end game of MMT is upon us. I do not worry much about these jackals “killing Bitcoin” due to this type of policy which actively prevents on/off ramping and pushes innovation offshore. Quite the contrary, I think this would actually speed up the development of a circular economy priced in Bitcoin exponentially.

Figure 2 above shows us the daily cluster which has gone mostly sideways during the month of May with some surprise dips and upside moves along the way. After breaking down under $26,000 and giving us reason to believe a retest of the $24,800 nPOC was in order (the $24,500 nPOC & gap in the weekly LVN cluster also in the area), Bitcoin found its footing and has since topped $28,000 on multiple occasions, clearing out some HTF nPOC and EI’s. Currently, Bitcoin is having trouble staying >$27,000 on subsequent moves higher with initial support coming in at $26,400, below there, $26,150 before the local lows of $25,800 are exposed and we face the possibility of another potential move downward towards the $24,800/500 area.

Personally, I am not sold on additional upside being totally out of the question for Bitcoin just yet. Failure at the $31,000 level has definitely made me reconsider some of my loftier targets, but so far, we have not broken down meaningfully under $25,000 and continue to find support well ahead of major lines in the sand. I am not thrilled that we failed twice up over $28,000, but am looking for another shot at it, and if it can hold, I am expecting the $28,550/$28,750 levels to give us some initial resistance. Getting above that area does expose us to the $29,600 nPOC pretty quickly.

Stepping down to the 4H, figure 3 shows us the current resistance levels that need to be cleared in the interim before we can even think about a retest of the $28,000 handle or beyond to my loftier targets. Over the past few hours, we have cleared the $27,100 nPOC, found some selling pressure, and an imbalance formed right around the current structures 4H vPOC. This was to be expected, and we covered it extensively in the alpha channel (available to advanced tier subscribers) on Discord in realtime. Currently, getting back above the 4H vPOC at $27,100 and clearing the sell imbalance located at $27,150 would be the first steps to ultimately clearing the $27,850 edge imbalance and giving us another shot at the $28,000 level again, more specifically, the $28,150 nPOC. There is a chance that we do stall in the LVN cluster located in the middle of the range between vPOC and the EI around $27,400/500. It is definitely possible to have that LVN filled out before any move higher (or potentially back lower) occurs, so make sure to keep an eye on how Bitcoin reacts once reaching this zone.

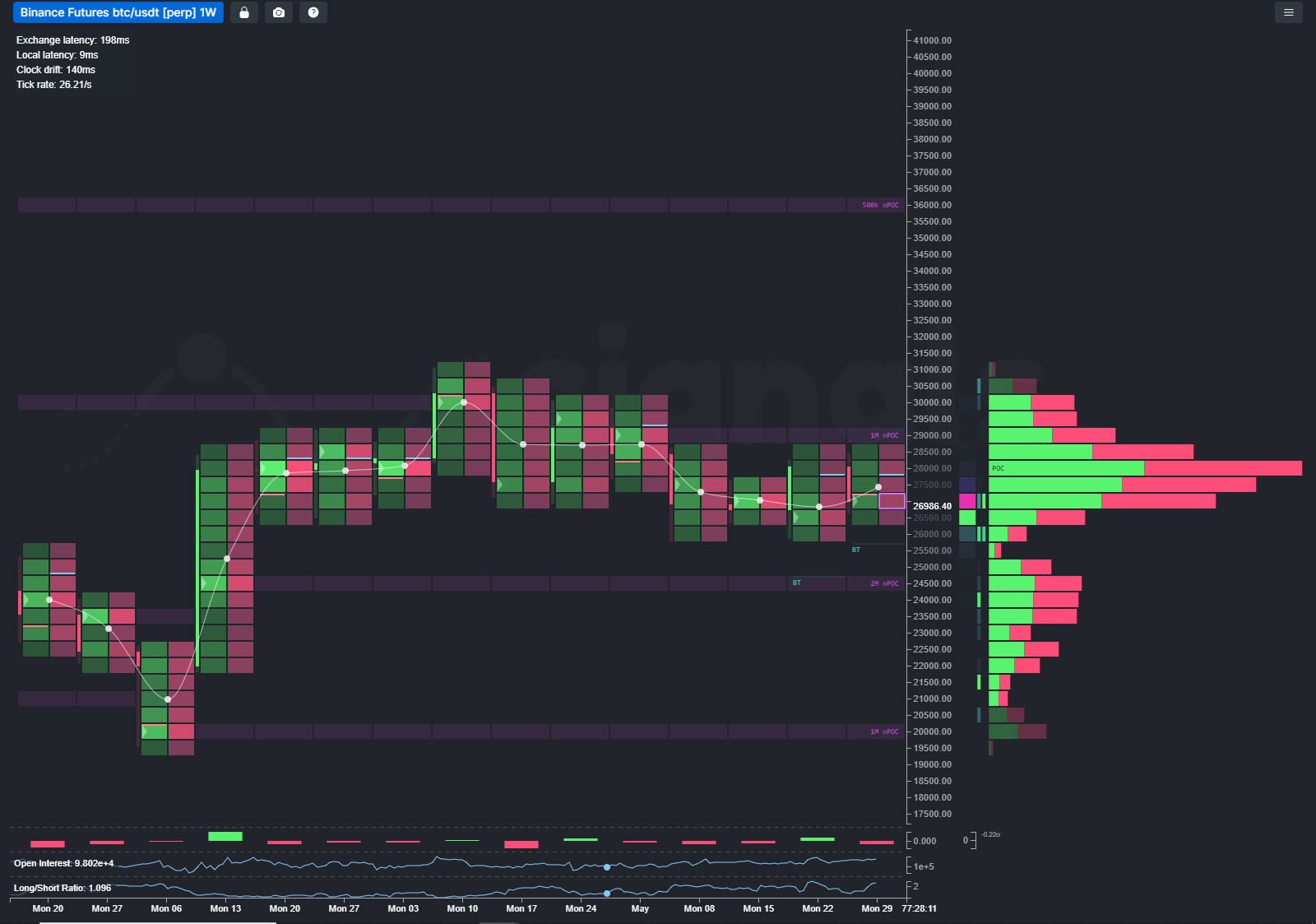

Last, we look at the weekly cluster as featured in figure 4 above. As you can see, we’ve been trading between two nPOCs for the better part of the last month. Notice, as stated above, the $24.5k area is of major importance if we started to break down. This area does not only host nPOC, but was one of the thinner parts of the profile left behind when Bitcoin made its first moves back over $30k. It’s been impressive that Bitcoin has held over $25,000 on all the pullbacks that have occurred lately. We do have two sell imbalances located right at $28,000, but with VWAP starting to turn up and provide support over the last two weeks, along with buyers showing interest via L/S ratio and OI beginning to pick up a bit, the prospects for a break towards $29,000-$30,000 can’t be ruled out yet, no matter how much bears may disagree (considering most of them were short the whole way from $17,000).

If we can retake the trend high of $31,000 and move past it, keep an eye on the weekly nPOC at $36,000 as this was my next point of interest >$31,000, crazy as that may seem. Conversely, if we did break down below the $24,500 area, the next major point of interest would be around $23,000/$22,500 and then the $20,000 nPOC. Again, I still believe there is a recession coming toward the end of the year, so any of these upside objectives would likely play out before that occurs. Once markets start unwinding it will get very violent, there is a chance that we could test under the $15,000 level during such volatility and find our true trend low before the next cycle kicks off. There is a major opportunity to make more Bitcoin during this process if you time everything correctly, so not over-trading and having patience is the key here!

Thank you for supporting Cignals & subscribing to our Substack! Don’t forget to check us out on YouTube, Discord, & Twitter as well! Make sure you check out our basic plan ($19/mo) which gives you access to all of our time frames, pairs, exchanges & many studies/indicators. Our advanced plan ($79/mo) gives you access to all of that, as well as the private Discord channels, API, even more studies, 1:1 coaching if needed, as well as early access to beta features. If you haven’t signed up for your free account yet, what are you waiting for?! Already a member and want to earn cashback? Ask about our referral program, where you get paid 25% of any revenue generated from your unique referral code.

***Any views expressed in the above are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.***

***Please also see our risk disclosure, linked here***